Malaysia’s HCP market sees declines

June 22, 2022

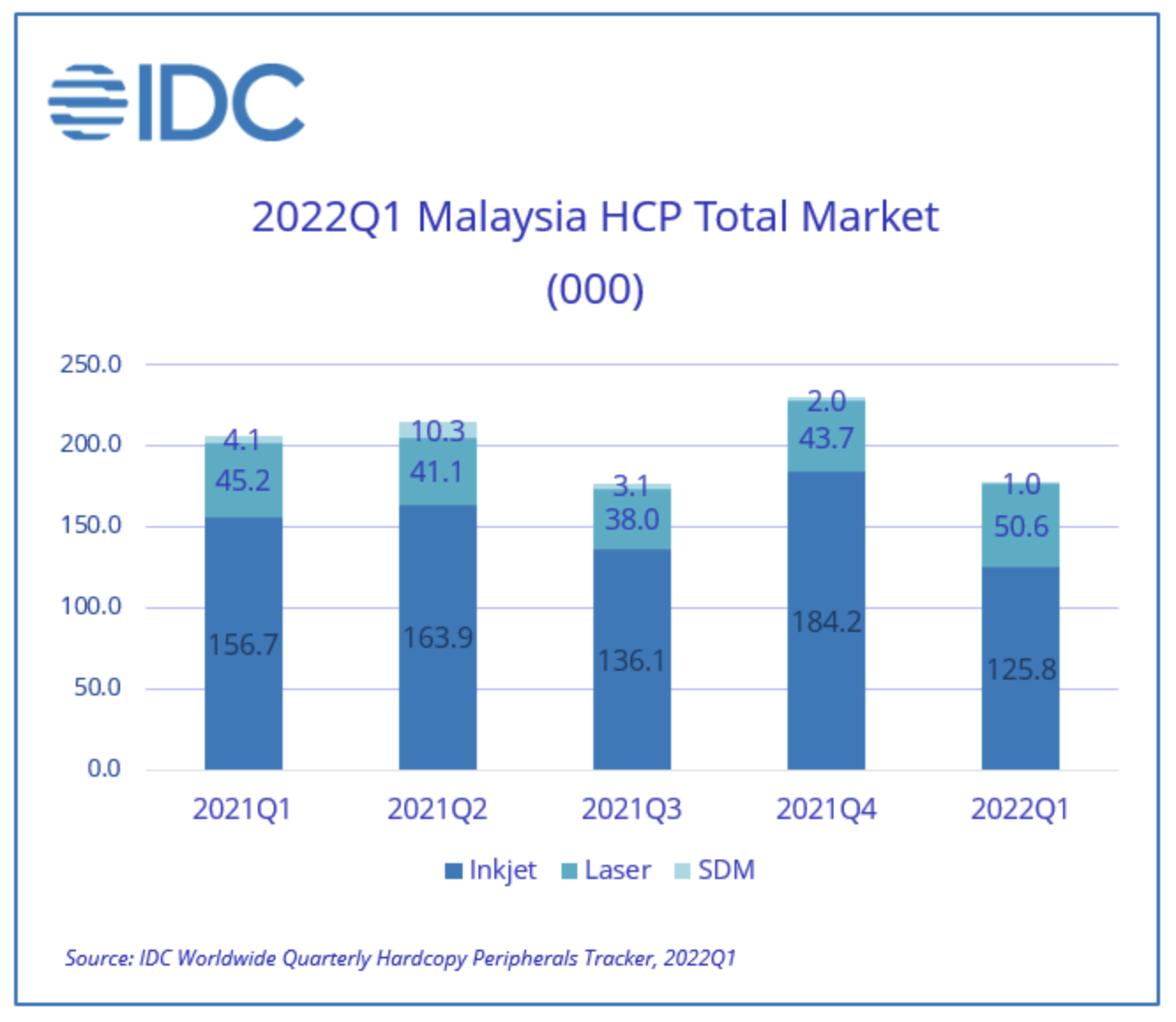

According to the International Data Corporation’s (IDC) Worldwide Quarterly Hardcopy Peripherals Tracker, including inkjet, laser, and SDM, the 2022Q1 overall market recorded a 13.9% year-on-year and 22.8% quarter-on-quarter decline.

This follows a market recovery in 2021Q4 driven lifting of pandemic restrictions and a resumption of business activity in Malaysia. Despite supply challenges, market recovery continues to be seen in the office segment for 2022Q2, meanwhile the home-printing segment has been a downward trend.

According to ID, the overall decline in 2022Q1 can be mainly attributed to the significant drop in the inkjet segment of 19.7% year-on-year and 31.7% quarter-on-quarter. This was in response to the large shipments in the previous quarter, which had a 24.1% growth year-on-year in 2021Q4, resulting in an oversupply of inkjet products in Malaysian markets. Additionally, strong market demand during the COVID-19 pandemic has begun to normalise as most offices are operating at full capacity and the work-from-home trend recedes in the short-term.

According to ID, the overall decline in 2022Q1 can be mainly attributed to the significant drop in the inkjet segment of 19.7% year-on-year and 31.7% quarter-on-quarter. This was in response to the large shipments in the previous quarter, which had a 24.1% growth year-on-year in 2021Q4, resulting in an oversupply of inkjet products in Malaysian markets. Additionally, strong market demand during the COVID-19 pandemic has begun to normalise as most offices are operating at full capacity and the work-from-home trend recedes in the short-term.

In contrast, the return of office activity led to a recovery in the laser segment, which grew 11.9% year-on-year and 15.9% quarter-on-quarter in 2022Q1. The recovery was supported by improvements in vendor inventory levels at the beginning of the year. However, the degree of inventory recovery differed among laser products, where continued shortages in A3 chips have led to the copier segment seeing slower quarterly growth at 13.0% and a year-on-year decline of 18.8%, whereas the laser printer segment has better results with higher growth quarter-on-quarter at 16.3% and year-on-year at 17.7%.

Supply constraints remain the primary factor for weaker performance in the copier segment and is expected to be prolonged as chipset shortages due to geopolitical tension and export restrictions in China’s major ports. IDC said that these challenges will continue to limit the ability of vendors to take advantage of improving market opportunities and impede recovery in the overall market. Additionally, market demand edges lower as existing clients increasingly request lease extensions for existing units and orders from the public sector remain sparse.

“The reopening of the Malaysian economy has shifted home-printing demand back towards offices, in turn this has shifted market imbalances from the inkjet segment towards the laser segment as demand outstrips supply,” said Eugene Lim, IPDS Market Analyst at IDC Malaysia.

Top 3 home/office printer brands highlights:

Canon maintains its position as the market leader in the overall home/office printer market for 2022Q1 holding a 40.3% share this quarter, however the brand sees a 6.3% decline year-on-year due to lower inkjet shipments for 2022Q1. This follows a substantially large shipment of inkjet models in the previous quarter which secured Canon’s position as market leader for 2021. Canon’s channel partners received a major replenishment of their inventory levels which has resulted in Canon lowering their inkjet shipments for this quarter to avoid over-supplying this segment, ultimately leading to a 21.9% year-on-year and 53.4% quarter-on-quarter decline in 2022Q1. Canon’s laser segment saw better performance with a 51.4% year-on-year growth, and a quarter-on-quarter growth of 24.0% driven by their mono models which have benefitted from office reopening and a relatively better supply situation compared to other brands. Their laser printer segment in particular saw a strong 23.5% rebound in growth following lower volumes over the past quarters due to shortages.

HP remains the second market leader with a market share of 29.1%, where they see an overall year-on-year decline of 25.3%. In response to high shipment volume in the inkjet market for 2021Q4, HP had lowered their inkjet shipments this quarter leading to a 28.7% decline year-on-year and a 13.9% quarter-on-quarter decline for 2022Q1. HP sees slight improvement in their laser segment with a quarter-on-quarter growth of 0.2%, with a strong performance for their copier models which saw a 40.7% quarter-on-quarter growth, however this follows a lower base volume and quarterly decline of 17.4% in 2021Q4. HP continues to face supply challenges due to chips shortages and their laser segment sees a 10.7% decline year-on-year.

Epson keeps its third position with a 18.8% market share with a quarter-on-quarter growth of 1.2%, though it sees a year-on-year decline of 13.3%. Epson continues to perform well even as inkjet demand falls as printing requirements are shifted from homes towards offices as their ink tank models benefit from recovering SOHO and SMB demand. The brand is not immune to supply challenges however where they encountered shortages even among their main models. Shortages are especially seen in their SDM segment which has seen an 81.8% year-on-year and a 60.6% quarter-on-quarter decline, which has benefitted their competitors in this segment who have picked up on orders they were unable to fulfil.

“Generally, laser printer vendors who were able to maintain good inventory levels were able to benefit from recovering demand in the segment. However, rising costs and falling print volumes will pose challenges towards demand,” added Lim.

Categories : Around the Industry

Tags : Business HCP Shipments IDC Market Research